Borrowers, investors, and industry observers have all taken notice of the Kennedy Funding Ripoff Report in recent years. Fast funding and flexible loan terms are hallmarks of Kennedy Funding, a direct private lender best known for its hard money and commercial bridging loans. It has, however, also been charged with poor communication and having unstated costs.

This article provides useful guidance for anyone interested in private financing while balancing the facts and myths. You may make wise decisions that safeguard your investments and financial future by being aware of the claims, the industry background, and the borrower protection procedures.

Who Is Kennedy Funding?

| Allegation Type | Description | Impact on Borrowers |

| High Upfront Fees | Non-refundable due diligence fees, often thousands of dollars | Loss of funds if loan not approved |

| Changing Loan Terms | Sudden adjustments to interest rates or repayment conditions | Increased repayment costs, project delays |

| Poor Communication | Delayed or no responses after fees are paid | Frustration, uncertainty during funding process |

| Lack of Transparency | Vague fee breakdowns or unclear contract terms | Difficulty in understanding true loan costs |

| Predatory Lending Allegations | High interest rates or restrictive clauses | Financial strain, risk of default |

Kennedy Funding is a private lender with a focus on asset-based financing and commercial bridging loans for customers in the Caribbean, Europe, and Latin America, in addition to the United States.

Since 1987, the business has marketed its capacity to fund complicated transactions that other lenders could turn down and to offer quick closings, frequently in as little as five days. It markets itself as a go-to option for borrowers in need of prompt, customized funding by providing loan sums ranging from $1 million to $50 million with adjustable conditions.

What Is the “Ripoff Report” About?

The Kennedy Funding Ripoff Report mentions online grievances and reviews in which borrowers express dissatisfaction. These frequently bring up exorbitant upfront costs, altered lending conditions, or a lack of openness. Some statements are specific, but others lack supporting evidence or context. It’s critical to realize that these allegations may combine misconceptions regarding hard money lending with legitimate worries. Borrowers are better able to determine whether a lender’s methods fit their demands and risk tolerance when facts are separated from conjecture.

Also read: Zaviluwazas: A Quick Guide to Smart Business Solutions

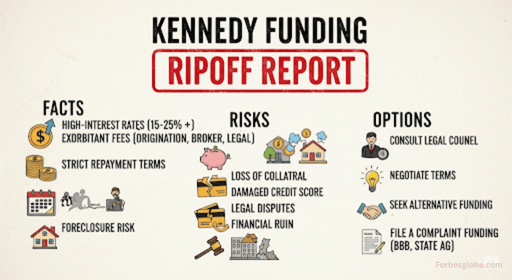

Common Allegations Against Kennedy Funding

A number of persistent grievances have been voiced by borrowers regarding Kennedy Funding. The most frequent ones are unanticipated modifications to loan terms, non-refundable due diligence fees that can amount to thousands of dollars, and inadequate communication following fee payment.

Predatory lending practices, such exorbitant interest rates or provisions that complicate repayment, are mentioned by others. These claims emphasize the need for care, even though some clients report successful funding. Before signing a private lending contract, prospective borrowers can identify warning signs by being aware of these concerns.

| Alternative Type | Key Features | Pros | Cons |

| SBA Loans | Backed by U.S. Small Business Administration | Lower rates, government-backed | Slow approval, strict eligibility |

| Credit Unions | Member-owned financial institutions | Competitive rates, local focus | Smaller loan limits |

| Peer-to-Peer Lending | Borrow from private investors via online platforms | Flexible criteria, fast approvals | May have higher interest for risky deals |

| Asset-Based Lenders | Loans secured by property or business assets | Fast funding, flexible terms | Higher interest rates |

| Regional Private Lenders | Smaller private lending firms with local market knowledge | Personalized service, potential lower fees | Limited geographic reach |

Industry Context – How Hard Money & Bridge Loans Work

When regular banks refuse to lend, short-term funding options like hard money loans and commercial bridging loans are frequently utilized. They offer speedy financing and flexible terms, although they usually have higher interest rates and upfront charges.

Analyze each clause in the contract, looking for any unclear or changing wording. Keep track of all written agreements, conversations, and emails. You can steer clear of expensive mistakes, dishonest lending tactics, or unstated expenses associated with specific problems by getting legal counsel before signing.

Analyzing the Complaints

It is evident from reading the Kennedy Funding Ripoff Report that not all allegations are equally serious. While some borrowers may have legitimate concerns, such as exorbitant upfront fees or last-minute term adjustments, others may stem from a misinterpretation of how private lending operates.

There are also positive evaluations that highlight successful funding for challenging projects and quick closings. Borrowers can distinguish between sporadic occurrences and regular trends by examining several sources. Making well-informed selections before signing a commercial bridge loan agreement is made easier with this well-rounded strategy.

Also read: What Is Fectayaznindus and Why Are People Talking About It?

The Regulatory Perspective

Private lenders like Kennedy Funding are subject to different regulations in the United States than traditional banks, which allows them greater flexibility but also less scrutiny. Kennedy Funding has not been penalised by any central regulatory body despite complaints about the Ripoff Report.

This implies that to protect themselves, borrowers must rely significantly on due diligence. Verifying a lender’s licensing, verifying prior transactions, and consulting with legal or financial experts before signing can all help to make the terms of a commercial bridge loan more fair and transparent.

How to Protect Yourself While Seeking Private Investment

Before speaking with any private lender, start by using a due diligence checklist. Request a detailed explanation of all costs and compare terms with at least two similar commercial bridge loan offers. Analyze each clause in the contract, looking for any unclear or changing wording.

Maintain a record of every written contract, discussion, and correspondence. By seeking legal advice before signing, you can avoid costly errors, dishonest lending practices, or undeclared costs related to specific issues.

Alternatives to Kennedy Funding

There are a number of funding options available if you’re not convinced about partnering with Kennedy Funding. Although approval takes longer, SBA loans from banks or credit unions can have lower rates. Platforms for peer-to-peer lending can link debtors with individual investors prepared to provide money to unusual initiatives.

Regional private lenders and asset-based lenders might offer favorable terms without the same up-front expenses. You may locate a commercial bridge loan or other funding solution that meets your needs by balancing time, cost, and transparency by looking into a variety of possibilities.

Also read: Koivaninbez Overview: AI, Blockchain & Cybersecurity Solutions

FAQS

What is the purpose of the Kennedy Funding Ripoff Report?

It is an online repository of complaints from borrowers who claim inadequate communication, fluctuating loan terms, and exorbitant costs.

Is Kennedy Funding a trustworthy lender?

Although it is a licensed private lender, some borrowers have had negative experiences; it is important to complete your research.

Why do borrowers at Kennedy Funding complain about hidden fees?

Some claim expenditures that weren’t fully disclosed prior to signing or non-refundable due diligence fees.

How can I stay clear of problems similar to those in the Ripoff Report?

Before making a commitment, compare several lenders, read contracts carefully, and ask for all fees in writing.

Are there any less risky options than Kennedy Funding?

Peer-to-peer lending, credit unions, SBA loans, and other asset-based lenders with clear terms are available options.

Final Verdict

Every borrower should take seriously the concerns raised by the Kennedy Funding Ripoff Report, particularly those about upfront costs, fluctuating terms, and communication problems. However, the company has also offered alternatives for speedy closings and transactions that many lenders reject.

The key is to engage in any private finance arrangement with caution; research your possibilities, weigh your options, and speak with an expert before committing. By combining careful due diligence with an awareness of potential risks, you can secure funding that advances your goals without causing unnecessary financial setbacks.